The 401(k) Alts Rule: History Repeating?

Paul Laughlin Jr. · LaughlinRE LLC · April 2026

If you have a 401(k) or savings with a brokerage firm, there's a category of investments - non-traded REITs (NTRs), non-traded business development companies (BDCs), and interval funds - you may never have heard of. That obscurity is partly by design. These products are complex, illiquid, and loaded with fees, which makes them extremely profitable for fund managers.

A proposed DOL rule (RIN 1210-AC38) may open the largest distribution channel these products have ever seen: the $12 trillion American retirement system.

What Are These Products?

Non-traded REITs own real estate; non-traded BDCs lend to private companies. Neither trades publicly. Getting your money back requires redemption queues (capped at 5%/quarter), IPO, merger, or liquidation - often 7-10 years out, sometimes never. Front-loaded fees historically ran 5-10%. Early distributions were often return OF capital, not return ON capital. Many investors didn't understand what they owned until they tried to exit.

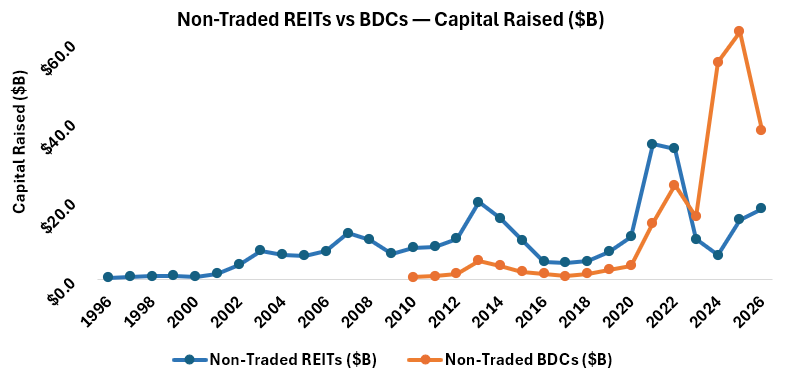

The Pattern (Repeated Once Already)

2007: Fundraising hits its highest peak yet: $11.7B.

2009: Great Recession and liquidity crunch results in fundraising decline to $6.5B (a 45% decline over a 2-year period).

2013: NTR fundraising peaks again, but higher at $19.8B.

2015-17: FINRA crackdowns; Ameriprise fined for 8,000+ unsuitable sales; fundraising collapses to $4.2B.

2018-19: Blackstone launches BREIT; wire houses re-enter under "institutional quality" branding.

2021-25: Record flows. Blackstone raises $24.9B in 2024 (68% of sector). BDC formation hits $63B in 2025.

2026: BDC sales down 49% from peak. Redemptions surge. Listed BDCs cut dividends. The product gets rebranded. The fees get trimmed. The distribution channel shifts. The underlying dynamic - illiquid assets sold on the promise of stable income - stays constant.

What the Proposed Rule Does.

Creates a six-factor safe harbor: performance, fees, liquidity, valuation, benchmarking, complexity. Document the process, receive judicial deference.

Key provisions:

ERISA doesn't require fully liquid options (investors may never fully liquidate - even in retirement)

Higher fees permissible if "justified by value"

Explicitly shields against "opportunistic trial lawyers"

What the Proposed Rule Doesn't Do.

Ameriprise's 2017 violations were retail brokerage (FINRA/state law) - not ERISA. This rule governs 401(k) plan menus, a separate legal framework. The same firms that retreated from retail now have a cleaner path into retirement accounts. The legal exposure is different. The products are not.

The Big Question.

Is this rule protecting savers through clearer standards - or clearing the legal runway for asset managers just as the retail cycle falters?

The six-factor safe harbor doesn't change what these products fundamentally are: illiquid, fee-intensive, dependent on liquidity events that may not materialize on schedule. What changes is the liability landscape for sellers. When liability shifts in favor of distribution, distribution follows.

The cycle has repeated twice in 15 years. If this rule passes, $12 trillion in retirement savings becomes the next frontier.