What are PIK Loans?

Ever hear of a PIK loan? Most people haven't, but they’re becoming quite the buzz word in today’s economy. Here's a simple breakdown of how they work and why they matter:

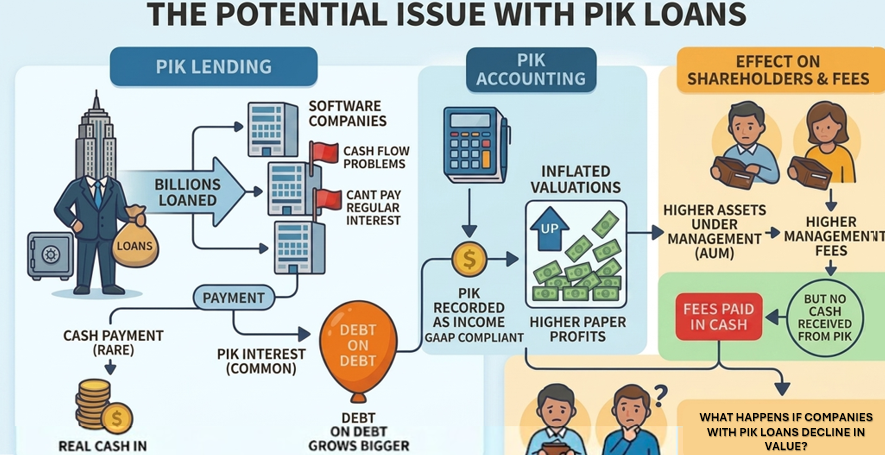

PIK stands for “Payment-in-Kind.” A borrower takes out a loan. Instead of paying cash interest, the borrower adds the interest to what they already owe. No cash changes hands. The loan balance grows over time instead.

So why do companies use them? They need capital to grow but can't afford regular interest payments yet. PIK loans provide breathing room. For a startup or a fast-growing software company reinvesting every dollar back into the business, that flexibility can be useful. It lets promising companies access capital they otherwise likely couldn't.

Lenders benefit too. The loan balance grows over time, which increases the value of the investment on paper.

It can get more nuanced, though. Under standard GAAP accounting rules, that accumulated interest still gets recorded as income, even though no cash was received. That paper income increases the size of the portfolio on the books, which can influence fund management fees. When the size of the portfolio increases as a result of those deferred PIK payments, so do the management fees, because portfolio fees are based on fixed percentages (1-2% of AUM).

PIK interest diagram

So the questions worth asking become straightforward: what happens if the borrower struggles to repay the loan? What happens if a company worth $80 million takes out a $60 million loan with an extra $10 million in PIK interest, and the company’s valuation drops to $55 million?

The recorded income gets revised and the investment value adjusts downward. Meanwhile, fees calculated during that period were based on the higher paper values, and they were paid in cash from the fund’s operations… so they don’t get reimbursed to the fund later on.

There's also a timing element worth understanding. Because PIK loans defer cash payments, early signs of borrower stress can be harder to detect compared to traditional loans where missed payments are immediately visible.

None of this makes PIK loans inherently good or bad. They serve a real purpose in the market. But as an investor in any fund holding them, understanding how they work helps you ask better questions before investing in funds with PIK loan concentrations.